Best Construction Insurance Companies in Florida for 2026

/Florida construction businesses carry a heavier insurance burden than almost any other state, and the Construction Insurance Companies you choose can either protect your operation or quietly drain it. Hurricane exposure, aggressive litigation, and carriers pulling back from roofing and demolition trades all make the stakes very real. Managing multi-party liability on large commercial projects adds another layer that most off-the-shelf policies were never built for. After reviewing dozens of providers serving Florida contractors, this guide breaks down the five strongest options worth your attention in 2026.

Behind the ranking

Publicly available information shaped every selection here: carrier reviews, AM Best financial strength ratings, service pages, and customer feedback pulled from multiple platforms. Only providers with a documented track record serving construction businesses made the cut.

→ See the full research breakdown

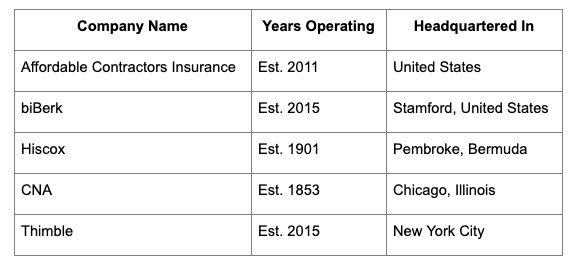

Affordable Contractors Insurance - Best for small to mid-sized contractors needing fast, trade-specific coverage

biBerk - Best for small business construction insurance

Hiscox - Best for small to mid-sized construction businesses and specialized trades

CNA - Best for construction and commercial property and casualty insurance

Thimble - Best for on-demand construction and trade business insurance

The Real Impact of Construction Insurance Companies

Choosing the wrong carrier in Florida isn't just an administrative headache. It can mean uncovered losses, failed contract requirements, or a workers' compensation claim that wrecks your experience modification rate (EMR) for years.

Florida contractors deal with challenges that most standard commercial policies don't fully anticipate. Carriers with a thin appetite for high-risk trades like roofing or underground utilities often exclude the exact work that makes up your main revenue stream. Then there's the multi-party liability exposure on larger commercial or public projects, where one incident can trigger claims across multiple lines and parties at once.

Specialized construction insurance companies understand how loss ratios shift between trade classes and project types. They price policies that reflect your actual claims frequency and severity per $1M in payroll, not a generic small-business average. That kind of precision matters when renewal time comes. The right coverage keeps your EMR manageable, your premiums predictable, and your contracts fully compliant.

5 Top Picks at a Glance

Note: All data in this table is sourced from review platforms and the official websites of the listed companies.

1. Affordable Contractors Insurance - Best for Fast, Trade-Specific Coverage

How Does Affordable Contractors Insurance Help Its Customers?

Affordable Contractors Insurance operates as a brokerage built around contractor needs. They cover general liability, workers' compensation, commercial auto, builder's risk, tools and equipment, and umbrella liability. The contractor-focused approach means they understand the compliance pressure that comes with certificate of insurance requirements on Florida job sites. Their same-day policy binding is one of the most practical features for contractors who need proof of coverage before a project kicks off the next morning. For small to mid-sized trade businesses, that kind of speed is rare.

What Sets Affordable Contractors Insurance Apart from Construction Insurance Companies?

Affordable Contractors Insurance solves one of the most common frustrations in the trade: the gap between needing coverage and actually having it in hand fast enough to keep a project moving. Same-day binding combined with genuine contractor knowledge (not just a generic small-business policy dressed up with contractor language) is what separates them from broader commercial insurance options.

Real User Sentiment:

Contractors who work with Affordable Contractors Insurance consistently point to the speed of certificate delivery and straightforward communication as standout qualities. Trade professionals appreciate working with a team that already understands roofing, plumbing, and HVAC risks without needing lengthy explanations. Honestly, that baseline knowledge saves time on both ends of the conversation.

2. biBerk - Best for Small Business Construction Insurance

How Does biBerk Help Its Customers?

biBerk operates as a direct-to-consumer insurance platform under the Berkshire Hathaway Insurance Group umbrella. They cover workers' compensation, commercial auto, general liability, business property, professional liability, umbrella, and cyber insurance. The direct model cuts out the broker middleman, which translates to real cost savings (up to 20% compared to traditional channels, according to the company). For small construction firms watching overhead carefully, that pricing difference adds up fast over a policy year.

What Sets biBerk Apart from Construction Insurance Companies?

The main problem biBerk addresses is cost and accessibility, along with the friction that small contractors run into when trying to get quality coverage without paying traditional brokerage markups. Backed by Berkshire Hathaway's A++ AM Best rating, their financial strength gives small construction businesses the carrier stability that larger general contractors expect from their subs.

Real User Sentiment:

biBerk has built a customer base of over 200,000 small businesses, and the recurring theme in feedback is how fast and uncomplicated the online process feels. Users who expected a complicated application were surprised by how quickly they moved from quote to bound policy. The Berkshire Hathaway connection also gives a lot of customers confidence they wouldn't get from a lesser-known carrier.

3. Hiscox - Best for Specialized Trade and Professional Liability

How Does Hiscox Help Its Customers?

Hiscox has been writing specialty insurance since 1901, which means their underwriting depth for niche construction risks is genuinely hard to match. They cover general liability, professional liability, cyber, property, marine, aerospace, and a range of specialized risks. For construction businesses operating at the intersection of design and build (think architect-led firms or engineering-adjacent contractors), their professional liability products are particularly well-suited. They serve over 600,000 small business customers globally and carry an A (Excellent) rating from AM Best.

What Sets Hiscox Apart from Construction Insurance Companies?

Where Hiscox earns its place is in professional liability coverage for architecture, engineering, and artisan subcontracting trades, a space where many standard carriers either exclude the risk or price it poorly. That kind of specialized underwriting appetite, refined over more than 120 years, is genuinely difficult to replicate.

Real User Sentiment:

Hiscox has collected strong recognition from the industry, including six "Insurer of the Year" wins in eight years from Insurance Times Awards. Customers value both the breadth of specialty products and the financial stability behind them. For contractors who operate in design-build or engineering-adjacent scopes, the professional liability depth here is hard to find elsewhere.

4. CNA - Best for Commercial Construction and Large Project Coverage

How Does CNA Help Its Customers?

CNA Financial Corporation has been operating since 1853, making it one of the most established commercial carriers in this comparison. They cover property, marine, workers' compensation, general and product liability, commercial auto, and loss-sensitive programs designed for larger operations. Construction has been a designated customer segment for CNA since 2011, which means their underwriting teams and risk management services are built around the real challenges of construction projects. They distribute coverage through independent agents, brokers, and managing general underwriters across the U.S. and internationally.

What Sets CNA Apart from Construction Insurance Companies?

CNA tackles the coverage depth challenge that mid-to-large contractors face when standard policies can't keep pace with multi-party project structures and complex liability exposure. As the seventh largest commercial insurer in the U.S., its carrier capacity on large projects is something smaller or newer market entrants simply can't match.

Real User Sentiment:

CNA's reputation in the construction space is built more on a long track record than online review volume, which reflects their commercial focus. Contractors working with CNA through independent brokers tend to point to claims handling and the breadth of available coverage options as the consistent strengths. That kind of depth matters when a large project claim surfaces.

5. Thimble - Best for On-Demand and Short-Term Coverage

How Does Thimble Help Its Customers?

Thimble pioneered on-demand general liability insurance, and its platform genuinely changed how small trade businesses think about short-term coverage. They cover general liability, professional liability, business owners policies, commercial property, workers' compensation, cyber, business equipment, and event insurance across more than 300 professions. Policies can be purchased by the job, month, or year, and the app makes the whole process fast enough that a contractor can bind coverage between a client call and showing up on site. Thimble is backed by Arch Capital Group, which adds financial credibility to the platform's flexibility.

What Sets Thimble Apart from Construction Insurance Companies?

Thimble solves the flexibility gap that single-project contractors and part-time trade businesses run into when annual policies don't reflect their actual work volume. Smaller contractors often end up either over-insured with annual policies they don't need year-round, or uninsured on short gigs because getting temporary coverage seemed too complicated before Thimble simplified it.

Real User Sentiment:

Thimble has over 621 reviews on Trustpilot, with 86% rated five stars, which is a strong signal for a platform in this niche. Users consistently mention how fast the quote-to-bind process runs and how accessible the app makes the whole experience. For the smallest contractors in Florida doing project-by-project work, that speed and simplicity is genuinely hard to match anywhere else (and the per-job pricing keeps costs honest).

How These Were Chosen and Verified

The Data Collection Phase Explained

Building the initial list started with a broad sweep across insurance directories, trade association resources, and business review platforms. Company profiles, service pages, and publicly available carrier information were gathered from official websites and third-party sources. The goal was to assemble a wide enough pool that no obvious option got missed before the filtering began. Special attention was paid to providers that named construction trades in their coverage descriptions, rather than generic small-business carriers who list contractors as an afterthought.

The Shortlisting Pass

Once the longlist was assembled, options without verifiable track records in the construction insurance space were removed. This meant checking that coverage descriptions matched real construction use cases and that customer reviews reflected actual contractor experiences rather than general business feedback. Review patterns were analyzed for consistency. Providers where feedback was too thin, too generic, or showed patterns inconsistent with construction-specific claims handling got cut at this stage.

Verification Pass

Each shortlisted company went through a cross-check between what their websites claimed and what independent review sources reflected. Where a company positioned itself as construction-focused, that claim needed to show up in the actual feedback from trade professionals. AM Best financial strength ratings were checked directly. Carrier's appetite for high-risk trades like roofing and demolition was noted as a differentiation point, given Florida's specific exposure profile.

Industry Recognition and Authority

Award history, trade publication mentions, and carrier partnerships were factored in as supporting signals. Hiscox's repeated "Insurer of the Year" recognition, biBerk's Berkshire Hathaway backing, and CNA's standing as the seventh largest U.S. commercial insurer all qualified as meaningful authority markers. These signals don't replace product quality, but they do confirm a level of market credibility worth considering when contractors are making coverage decisions that affect their licenses and livelihoods.

Evidence Specific to Construction Insurance Companies

The final filter required each company to show genuine, documented relevance to construction insurance. That meant dedicated service pages covering construction trades, verified feedback from contractors and subcontractors, and coverage language that addressed real jobsite risks. General commercial carriers without construction-focused positioning didn't make the final list, even if their products could technically cover a contractor. The distinction between a carrier that can cover construction and one built around it matters for Florida contractors working through complex project requirements.

What to Look For When Choosing Construction Insurance Companies

Start by asking whether a provider actually understands your trade, not just commercial insurance as a whole. The gap between a contractor-focused carrier and a general small-business policy shows up fast when a claim gets filed.

Industry/Domain Experience: Look for carriers or brokers with documented experience in your specific trade. A roofer and a general contractor face very different underwriting profiles, and the right provider knows that without needing an explanation.

Features and Service Options: Check that the coverage menu matches your real needs: general liability, workers' comp, builder's risk, tools and equipment, and umbrella coverage should all be available under one relationship if possible.

Pricing Structure: Understand whether you're paying for annual coverage you may not need year-round, or whether flexible options like per-job or monthly policies better match your workflow.

Results Measurement: Ask how a provider tracks claims resolution time and certificate of insurance turnaround. Those metrics tell you more about day-to-day reliability than any marketing page.

Industry Knowledge and Compliance: Florida has specific state Department of Insurance regulations and licensing requirements for contractors. Your insurance provider should know those requirements and help you stay compliant without you having to chase the details yourself.

Final Take

Florida contractors don't have the luxury of picking coverage casually. Between the state's litigation environment, hurricane exposure, and carrier selectivity around high-risk trades, the Construction Insurance Companies you work with directly affect your project eligibility and long-term premium trajectory. Affordable Contractors Insurance fits well for fast, trade-specific needs. biBerk and Thimble work for cost-conscious smaller operations. Hiscox earns its place in specialty and professional liability. CNA carries the weight for larger commercial programs. As Florida's construction market keeps growing, so does the importance of getting the coverage match right from the start.